The Montrose, Denver, and National Housing Market

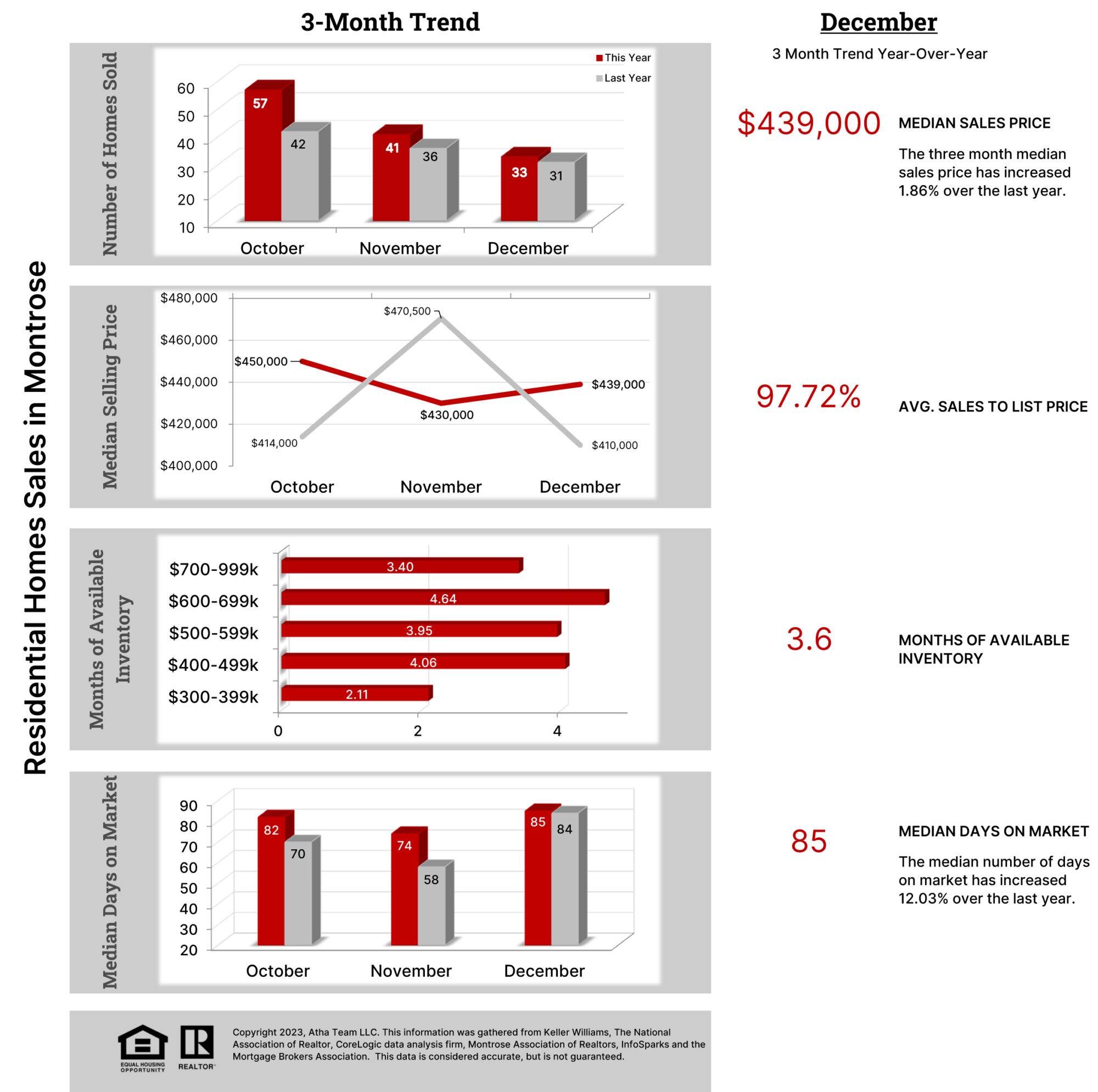

The Montrose real estate market just finished its second worst year since 2015. The Western Slope is faring better than the national real estate market, which just had its worst year since 1995. Overall, both local and national markets are stagnant due to a combination of elevated home prices and high interest rates. A 30-year fixed mortgage is now topping 7%. Home prices are still holding steady, with the median sale price for a home in Montrose increasing 6% to $439K over the last 12-months.

Housing inventory in our valley currently sits at 5-months of available inventory. Therefore, prices are expected to remain sticky unless inventory increases and then holds for a significant period of time. A market typically experiences price declines when housing inventory tops 6-months for a steady period of time. Some experts are predicting a price decrease in markets, such as Denver, that experienced annual double digit increases during the pandemic market run.

Denver Colorado is our primary source of home buyers moving to the Western Slope. The Denver market is also flat, with relatively few homes selling and with a slowly increasing inventory. We’ve had clients from the Denver Front Range not able to consummate purchases here in Montrose due to contingent homes not selling in Denver.

Supply and demand rule the markets, and therefore it’s unrealistic to expect real price decreases in Montrose unless inventory seriously increases.

Real Estate Market Predictions for 2025

Everything hinges on interest rates. Many banks and commercial real estate investors were chanting the mantra, “survive until 25”, expecting a significant decrease in the cost to borrow money (interest rates) and be able to restructure commercial debt. Residential real estate firms were also hoping for lower mortgage rates in 2025. Sadly, this mantra has become a false hope as interest rates for commercial and residential real estate are still very elevated.

The Federal Reserve’s small reductions in the federal funds lending rate has not had the expected effect on the 10-year treasury bond or mortgage rates. Therefore, we’re expecting 2025 to be a repeat of the previous year in the residential housing market, along with increased stress in the national commercial real estate sector. Unless there is a serious retreat from stocks toward bonds, and/or a recession, we expect rates to stay high, and for residential real estate markets to remain on their current trajectory.

Click Here to View Residential Sold – December