For those of you following our monthly stats that we produce in-house, we may sound like a broken record. Aggressive appreciation and price gains, supply and demand, multiple offers; this has become all too familiar.

Could there be a change in the wind? The recent interest rate hikes are not just announcements you hear on the news anymore, they are now translating to numbers on the closing table as buyers enter the realm of homeownership. All the while, paying approximately 30% more a month on average simply in interest from what they would have been paying a mere 4 months ago. It would stand to reason that we should start to see some significant changes in the real estate market because of this. However, reading our stats from April, it is clear that things are still extremely competitive in Montrose. We recently put a home on the market in Montrose for under 400k. We received between 15-20 showing requests within the first hour of it being live on the market. This vignette would suggest that there is still an extremely large buyer pool in the ‘lower’ price ranges in Montrose and that things are as competitive as ever. Despite the recent hikes in interest rates, homes are still selling for over asking price in Montrose.

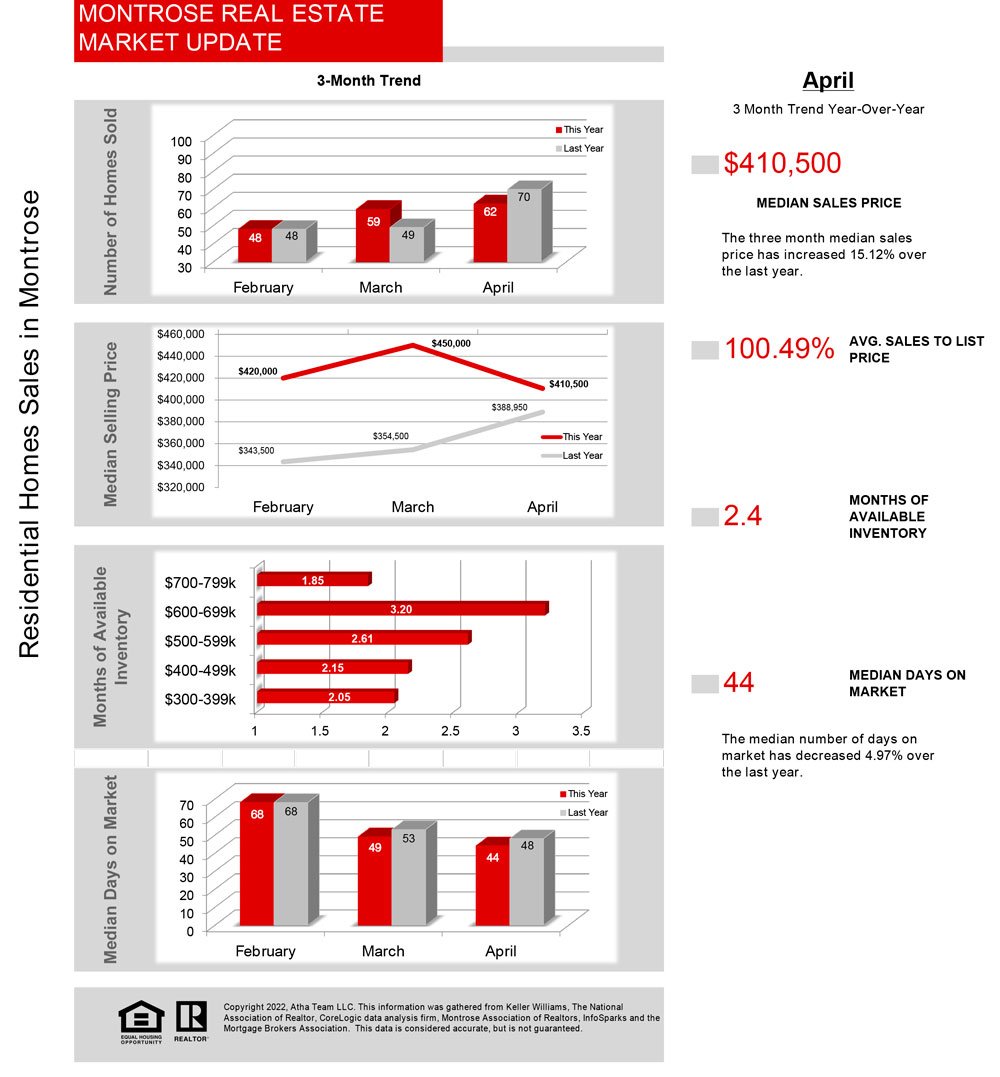

Taking a look at the higher-end market, notice the ‘median days on market’ price ranges box. $700-799k actually has the lowest amount of time on the market. This should tell us something interesting. It might be tempting to forecast a ‘doomsday’ for Montrose real estate because of rates and constant fear-mongering. However, it’s important to keep in mind that an extremely high amount of buyers in Montrose are coming from out of town, bringing their significant equity and/or cash with them, and are not concerned with interest rates in the way that a first-time homebuyer would be. As one of my buyers recently said as we wrote an offer, “I couldn’t care less what rates are, I just want to live in Montrose.” While this certainly isn’t welcome news to the first-time homebuyer in Montrose, it could likely function as a ‘hedge’ against a potential real estate downturn.

National Market

Widening our focus to the national level, it appears that things are not slowing down there either. 70% of markets in the US have seen even greater appreciation than last quarter according to the National Association of Realtors. Part of the reason for this could be the ‘mad dash’ to secure an interest rate in the 3’s or 4’s, as rates surged over the first quarter of 2022.

It could also be that now buyers are having to adjust their expectations in terms of what they can afford, considering most rates we are seeing today are in the 5’s and seem to be on the rise yet again due to the Fed’s announcement last week. In reality, buyers must either radically adjust expectations of what they can get for their budget, or they’re simply wrapping their minds (and wallets) around devoting more of their income directly to their mortgage. With home prices continuing to appreciate at a high pace, as well as interest rate increases, it is safe to assume that many homebuyers are now stomaching well above the traditional 28% mortgage debt to income ratio recommended by lenders. If they weren’t, we would likely begin to see more price reductions on existing home sales, but this has not been the case. You have to pay to play the game, and it could be that the modern home buyer is trading in their daily Starbucks mocha in order to compete in this high-priced, high interest rate-ridden market we find ourselves in.

Thinking about Buying or Selling? Call or Text: 970-417-9375

Statistics gathered from CREN MLS, criteria are all residential not including mobile or manufactured housing in Montrose. If you have a brokerage relationship with another agency, this is not intended as a solicitation. Equal opportunity housing provider. Each office is independently owned and operated. For sale by owner data not included in research findings. Sales data reflects sales from homes not limited to the Atha Team LLC. This information was gathered from Keller Williams, The National Association of Realtors, CoreLogic data analysis firm, Montrose Association of Realtors, CMU Department of Business and Economics, InfoSparks, YCharts, National Association of Realtors, Cornerstone Home Lending, and the Mortgage Brokers Association. This data is considered accurate but is not guaranteed. Copyright Atha Team LLC 2022. All Rights Reserved.

Get Our Hyper Local Real Estate Market Report Direct to Your Inbox

By clicking “Submit” you agree to receive marketing calls, text messages and/or emails from Atha Team regarding the potential purchase, sale or lease of real estate at the phone number and/or email provided, including by using automated technology, and understand that this consent is only for brokers or staff associated with Atha Team and no other companies.

Widening our focus to the national level, it appears that things are not slowing down there either. 70% of markets in the US have seen even greater appreciation than last quarter according to the National Association of Realtors. Part of the reason for this could be the ‘mad dash’ to secure an interest rate in the 3’s or 4’s, as rates surged over the first quarter of 2022.

Widening our focus to the national level, it appears that things are not slowing down there either. 70% of markets in the US have seen even greater appreciation than last quarter according to the National Association of Realtors. Part of the reason for this could be the ‘mad dash’ to secure an interest rate in the 3’s or 4’s, as rates surged over the first quarter of 2022.