As I reviewed the stats this week, one thing really surprised me. Every single line and bar graph looked almost identical to this time last year.

A few examples tell the story:

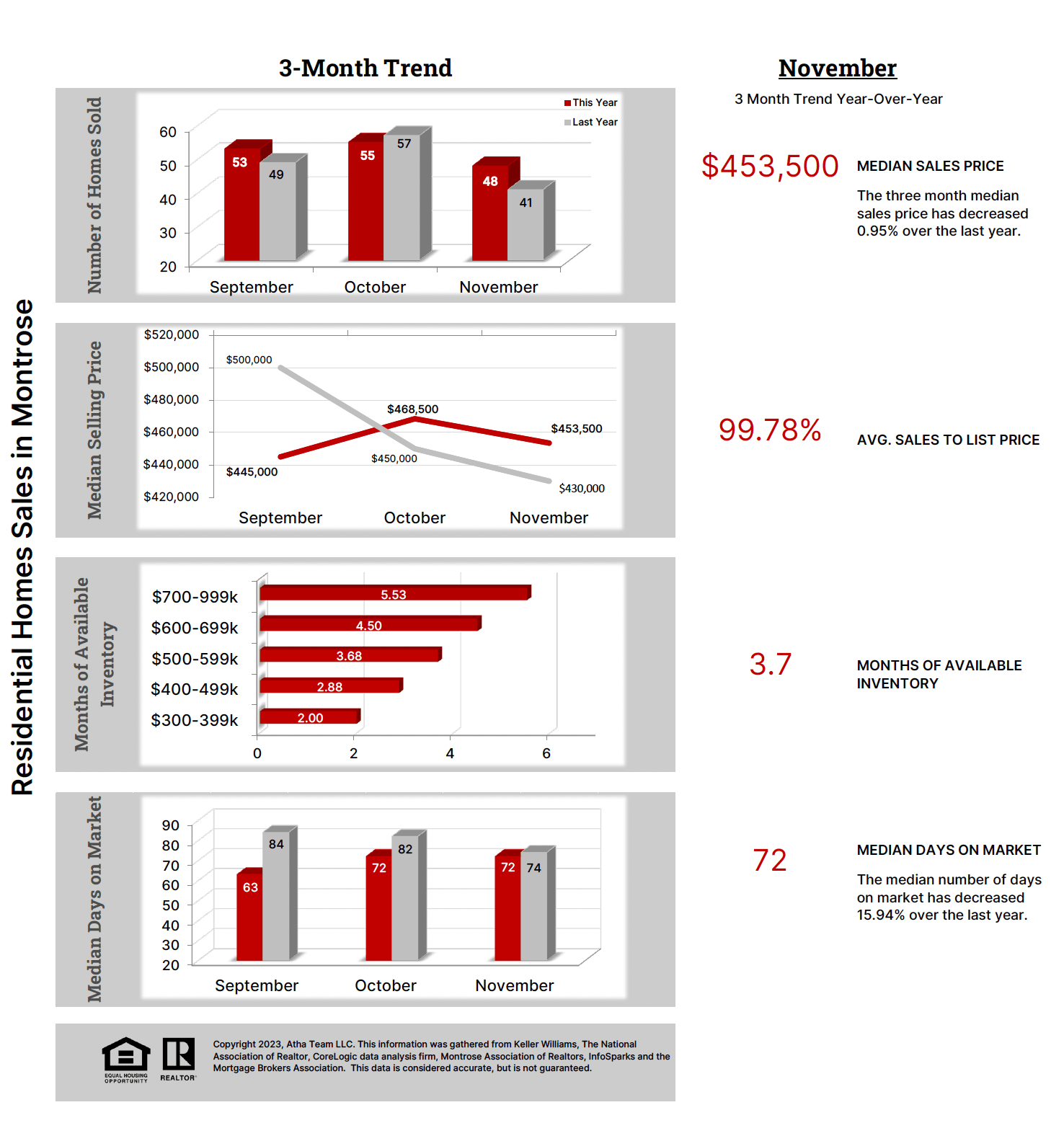

Days on Market

2024: 74 days

2025: 73 days

Under Contract

2024: 38

2025: 37

Showings to Under Contract

2024: 10

2025: 9

New Listings

2024: 46

2025: 46

I could keep going, but you already see the pattern. November this year looks a whole lot like November last year. There were too many similarities for it to be a coincidence, so I dug in to see what could explain a market that is almost a carbon copy of last year.

I didn’t have to look far. The logical place to start is interest rates. Rates are sitting at a four year low, hovering around 6.25 percent for a 30 year conventional loan. The decline began in September of this year, which is the exact same month they dropped to their previous lows in September of last year. The reason this November feels so familiar is simple. The biggest market driver we have started moving at the same time two years in a row, and the market reacted in nearly the same way.

So if November looks identical, does that mean 2026 will meander along like 2025 and 2024? I don’t think so. The key difference is that last year the Fed only dipped a toe into lowering rates before sending them right back into the high sixes and low sevens. This year is different. The lower rates have stuck. It is not the free money era of the post recession or pre covid years, but it is meaningfully lower than the highs we just lived through.

Based on that, I would argue that even a modest improvement in under contracts and days on market in December compared to last year would be a bellwether for a significantly healthier market in 2026.

Why Fed Cuts Don’t Always Cut Your Mortgage Rate

The Fed meets again today and I have had no fewer than five people tell me they expect Powell to announce lower rates. That is a reasonable expectation, but a discount in the Fed rate does not always translate to a matching drop in mortgage rates.

The last time the Fed made cuts, mortgage rates barely moved. Why? Because if lenders are confident a cut is coming based on the signals they are seeing, they will often price that cut into today’s rate before the Fed officially announces anything. In other words, the market reacts early. So even if we see another Fed cut, the mortgage rate you get may not fall much if lenders have already baked that sugar into the mortgage cake.

I bring this up because I keep hearing people say they plan to wait for the Fed meeting before they buy or refinance. The reality is that the rate you are seeing today is already a reflection of any action the Fed is likely to take. Waiting rarely gives you the advantage people imagine.

We saw this exact mindset last year. Folks told me they were holding off because they were sure rates were about to drop. Instead, the opposite happened. Rates popped right back up even though the smoke signals suggested they were headed down.

All that to say, timing the market based on Fed meetings is usually a losing strategy. If the numbers make sense for you today, then today is probably your smartest window.

Click Here to View Residential Sold – November

{kind=link}