Every time I look at our local real estate market, I have the same instinctive reaction: this must be unique to us. How could it not be? We’re a small, rural, retirement-leaning community, with the Montrose School District as the largest employer. While we’re influenced by the same macroeconomic forces as everyone else, like interest rates, it feels logical that our headwinds and tailwinds would produce a market unlike almost any other.

And then I read the headlines.

What quickly becomes clear is that there’s very little unique about what we’re experiencing. Nearly everything we’re feeling firsthand is being felt across markets all over the country.

Agents everywhere are dealing with a stale market. The same dusty listings have lingered since mid-summer, stubbornly clinging to pricing while the market sends sellers very clear, wax-sealed messages that they’re priced too high.

Everyone is feeling the gap left by first-time homebuyers. Higher interest rates, elevated prices, and limited inventory have made affordability a nationwide challenge, pushing young professionals to rent longer and delay homeownership.

And everyone is hearing the same refrain: buyers and sellers waiting. Waiting for rates, prices, construction costs, or land values to move in a more favorable direction before making a decision.

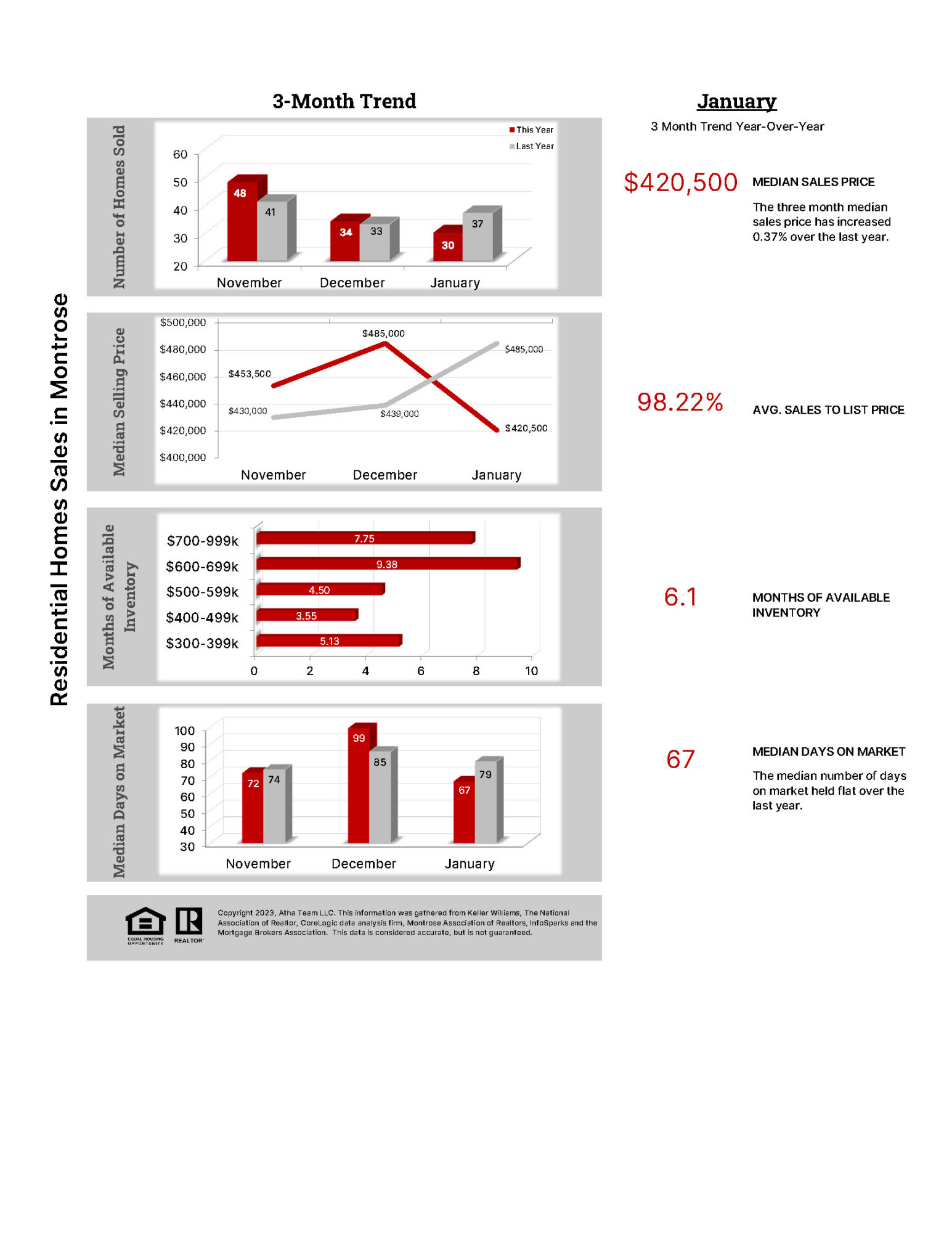

If you poured over last month’s market stats report, you may remember me saying that even a modest increase in unit sales over December and January would likely be a bellwether for a significantly improved market in 2026.

Well… that didn’t happen.

December saw just one more sale than the year before, and January actually saw seven fewer sales. Despite all of that, the market continues to move.

Not at the breakneck pace we became accustomed to during the COVID era, but it is moving. Average days on market dropped meaningfully from December to January, from 99 days to 67 days. Entry-level home sales led the market in January, pulling the average sales price down from $485,000 to $420,000. Inventory currently sits at 6.1 months, a level most would describe as balanced.

In short, the early smoke signals suggest 2026 will be more of the same. A moseying market with modest 3 to 6 percent appreciation and well-marketed, well-priced homes selling with relative ease.

Death of a First-Time Homebuyer Salesman

This past weekend, we had a couple of my wife’s younger cousins in town, both early in their careers, and they asked me for investing advice. I told them what I tell almost everyone: stop renting and buy a home.

I was promptly laughed out of the room.

One lives in Los Angeles, the other in the Denver metro area. That’s where the jobs are, so they’re logical places to start a career. One said it would literally be easier to buy a Lamborghini and live in it than to buy a home. The other explained that when he ran the numbers, his mortgage payment would be more than double his current rent for a comparable home in the same neighborhood.

I knew things were tough for first-time buyers. I didn’t realize just how out of touch I had become. And for the record, I’m the best buyer’s agent in the country, for goodness’ sake.

That conversation forced me to compare my first home purchase to what first-time buyers face today.

When I bought my first home in 2014, my interest rate was 3.5 percent. The home cost $136,000, and my total monthly payment, including a $200 HOA, was about $900. I used a low-down-payment loan and poured the money I saved into a full remodel, hiring contractors who were eager for work because the trades were struggling to stay busy.

That same home today sells for roughly $420,000. The interest rate this month would be around 6.11 percent. Using the same low-down-payment loan, the monthly payment jumps to roughly $3,317, again including the $200 HOA. And good luck getting a contractor to return your call for a small townhome remodel.

It’s no surprise first-time buyers feel like homeownership is out of reach. That said, it isn’t all doom and gloom.

Opportunities still exist for buyers willing to make compromises on their first purchase in order to create an entry point and start building equity. Almost no one buys their dream home on the first try. A first home should be purchased with the understanding that it likely isn’t forever, unless you’re Ryan Gosling in The Notebook and plan on rehabbing a teardown Victorian into a multi-million-dollar hobby farm. In that case, carry on.

One of the biggest hurdles I face with first-time buyers is helping them understand that options do exist. They just don’t look like a 3,000-square-foot home on 400 acres with a fully operational unicorn ranch. In many cases, the best starting point isn’t a single-family home at all. Last year, the median condo and townhome sale price was roughly $160,000 lower than the average single-family home, with several move-in-ready units selling for as little as $225,000.

These properties represent excellent entry points. They provide a place to live, an opportunity to build equity, and a path toward a future move-up or dream home.

Homeownership may be harder than it’s ever been for first-time buyers, but with realistic expectations and the right strategy, it’s still achievable.

Click Here to View Residential Sold – January

{kind=link}